The Pay to Stay work tax

Posted: October 29, 2015 Filed under: Housing benefit, Pay to stay, Social housing | Tags: National Living Wage Leave a commentOriginally posted on October 29 on Inside Edge 2, my blog for Inside Housing

The impact assessment of the Housing Bill reveals two devils buried in the detail of proposals for a compulsory Pay to Stay.

First, the principles. The assessment says ‘the Government believes that those on higher incomes should not be subsidised through social rents’. There are 350,000 social rented tenants with household incomes over £30,000 a year including 40,000 with incomes over £50,000. Higher rents for these High Income Social Tenants (HISTs) are justified by the fact that they ‘benefit from a subsidised rent that could be as much as £3,500 less, on average, compared to equivalent rents in the private sector’. Needless to say, neither of these figures is sourced. The government has form when it comes to changing its estimates of high earners (not to mention statistics in general) but:

‘This intervention is designed to remove an unfair subsidy. Households with a sufficiently high income do not require this, as they are able to access market housing.’

For the purposes of this blog, I’ll ignore most of the arguments about who really gets subsidised housing. But I can’t resist pointing out three things. First, on this basis the more the government makes a mess of housing policy in general, pushing up house prices and rents, the more social tenants are ‘subsidised’. Second, this policy has come a long way since it was said to be needed to stop people like Bob Crow and others earning more than £100,000 benefitting from social rents. Third, another part of the Housing Bill legislates for first-time buyers under 40 to get a 20 per cent discount on new homes worth up to £450,000 – you’ll need to earn almost £100,000 to benefit from that subsidy.

The assessment looks at the broad impacts while consultation continues on details such as the best way to administer the scheme and how to taper the income thresholds. It uses the same assumptions used in modelling for the Summer Budget: that households on incomes of £40,000 or more (£50,000 in London) will pay 100% of the market rent; while those on £30-£40,000 (£40-50,000 in London) pay 80% of the market rent. These assumptions reveal far more about the potential design of the policy than consultation papers published up to now.

Given the huge differences between social and market rents, the implications of this are already alarming enough for people who will not have considered themselves as high earners up to now. But could it get even worse?

The first devil in the detail is what counts as ‘income’. The last consultation paper defined it as the taxable income of the two highest-income individuals in the household. However, an eagle-eyed Joe Halewood has spotted that footnote in the income assessment says that the one assumed in this modelling is gross household annual income as described in the glossary of the English Housing Survey. This includes all income of all people in the household, including benefits and tax credits as well as earnings. As a quick illustration of the difference this seemingly technical change makes, a couple with two children earning £25,000 currently qualify for another £5,000 in child tax credit and child benefit, potentially making them a HIST. The footnote does add that ‘different definitions of household income will be considered for the detailed policy design following consultation’ but that remains to be seen.

The second devil is the way the income thresholds are set. The assessment assumes that Pay to Stay will initially affect 130,000 local authority households and 160,000 housing association households (based on 2012/13 incomes). However, it adds that:

‘As earnings increase over time, households who are currently beneath the thresholds at which higher rents are charged will break through the thresholds and be added to the higher-income cohort.’

Translated, this means that the £30,000 and £40,000 thresholds will NOT be uprated for inflation. An additional 70,000 local authority and 80,000 housing association households will be caught by Pay to Stay by 2017/18 because of increases in earnings in the meantime and more will fall into the net each year after that.

That’s crucial to bear in mind when it comes to the costs and benefits of the policy. The assessment estimates social landlords will incur £45m in transitional costs and £28m a year in admin costs. By my calculations, that means the government thinks landlords can administer the scheme for just £62 a year per tenant affected – wishful thinking? There will be additional unspecified costs associated with sharing income data with HMRC.

Next it comes up with figures for increased rental income and behavioural responses by tenants that may reduce it. Extra local authority rents go back to the Treasury but housing associations keep their increased income. The assessment does not include the effects of a taper but it does make assumptions about actions by tenants that could reduce this. Examples include increased rent arrears, movement out of the sector through choice and affordability, tenants reducing their income to avoid the thresholds or exercising the right to buy (perhaps the easiest way out for anyone who can afford it and not of course in any way a subsidy). It’s not hard to think of others but I’ll go with these assumptions for now.

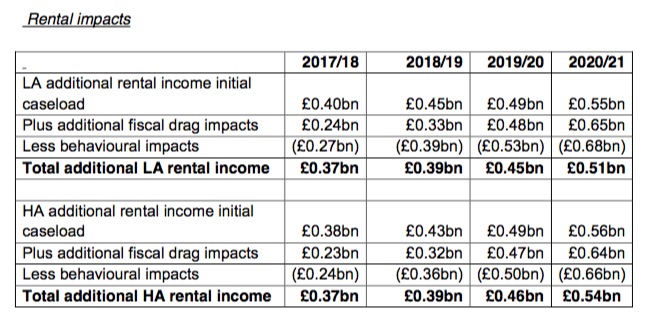

This table from the income assessment presents the best guess on the likely rental income less behavioural impacts:

As Inside Housing has already reported, social landlords’ net rental income will increase by a combined £1bn by 2020/21, split evenly between local authorities and housing associations. However, look a bit closer and something else emerges very clearly. Behavioural impacts will wipe out all of the extra income from imposing Pay to Stay on the initial caseload of tenants (those with higher incomes at the time the policy was first proposed). All of the extra income comes from fiscal drag, which means not increasing the thresholds in line with earnings.

On the assumptions used in the impact assessment, this means tens of thousands of tenants who may not think they earn enough to be ‘High Income Social Tenants’ will eventually be caught by Pay to Stay. Eventually, if the thresholds are not uprated, it will hit people most people would consider to be on very low incomes. As an illustration, the National Living Wage will be £9 an hour by 2020. A couple with one full-time earner and one working 24 hours a week would hit the £30,000 threshold. Worse still, if the definition of ‘income’ includes benefits and tax credits (as implied above) Pay to Stay would hit a couple with one full-time earner and one working 13 hours a week.

The policy will already hit people like nurses, paramedics and teachers who are social tenants. But as the National Living Wage rises most social tenants who are in full-time work will eventually be paying market or near market rents. This could turn into not just a tax on aspiration but on work itself – a second tax on strivers to follow the tax credits debacle.

To put this into perspective, the National Living Wage is of course just a rebranded National Minimum Wage for the over-25s. It is lower than the actual Living Wage, which is carefully calculated on the basis of what it actually costs to live. Yet the Living Wage is calculated on the assumption that people with children live in social housing paying a social rent. Pay to Stay turns that on its head: in a few short years it will have gone from being all about Bob Crow and Frank Dobson to something that affects most tenants in full-time work. The ambitious plans of right-wing think tanks to restrict social housing to the elderly and vulnerable will be close to fulfillment (today’s news on the end of lifetime tenancies only confirms this).

Worse still, unlike conventional means testing, Pay to Stay only takes account of incomes. No allowance is made for outgoings. That means the worst impacts are likely to fall on people with children and people with disabilities who are in work.

And what about the impact on affordability and housing benefit? As analysis by Savills for Inside Housing pointed out last month, tens of thousands of tenants will find market rents unaffordable. The assessment admits the potential impact of on housing benefit. Under the current system this would definitely be the case: a couple with two children earning £30,000 whose rent increased from £110 to £160 a week would get around £11 a week back in housing benefit. The same couple paying a rent of £220 a week would get £71 a week back. The cost will be even higher than that in London and the South East.

The assessment breezily claims that:

‘Following consultation on the detail of the policy, it is anticipated that intermediate thresholds and tapers may be able to avoid including many of those tenants receiving housing benefit (or who would float on to it if their rents increased).’

But how is that possible in a scheme that the impact assessment implies will extend so far down the income scale by 2020? If it is possible, won’t it mean a significant reduction in the extra income going to landlords? And if it does mean that, isn’t a policy that will condemn hundreds of thousands of tenants to higher rents likely to be an expensive waste of time?