Taxing questions for the housing strategy

Posted: June 11, 2026 Filed under: Home ownership, Stamp duty, Tax Leave a commentOriginally written as a column for Inside Housing.

Sooner or later a government will have to grasp the nettle of reforming the way that housing is taxed.

Sooner is the implication of Andy Burnham’s still semi-declared campaign to be Labour leader and prime minister, with the would-be MP for Makerfield keen to reform ‘regressive council tax’ and saying that he believes that land is ‘under-taxed’.

Soon, says the all-party Housing, Communities and Local Government (HCLG) Committee, in a report this week calling for reform of stamp duty land tax to improve affordability and a review of other property taxes.

Later has been the answer from all previous governments as they look at the implications of reforming stamp duty, council tax and inheritance tax and see a political minefield ahead of them.

But it’s had to imagine a long-term housing strategy that does not include reform of property taxes, which may be one big reason why the timetable for the one expected from this government has slipped so much.

First promised ‘in the coming months’ in July 2024, the strategy has been scheduled for ‘the new year’, ‘the spring’ and then ‘later this year’ in 2025, then ‘in the spring of 2026’. The current position, almost two years into the Labour government, is that it will be published ‘in due course’.

Read the rest of this entry »What will the Budget do on tax and housing?

Posted: November 5, 2025 Filed under: Budget, Stamp duty, Tax Leave a commentOriginally written as a column for Inside Housing.

With three weeks to go until the Budget, speculation is mounting about potential tax increases on housing.

Hemmed in by a manifesto that ruled out increases in rates of income tax, national insurance and VAT, the chancellor will have been looking at other options like council tax, stamp duty, capital gains tax and inheritance tax.

Rachel Reeves offered few specifics in her speech on Tuesday morning but it seems clear that tax increases are on the way that could have far-reaching effects on housing.

But while it’s easy to think of changes that might raise more money or be electorally popular, or make the tax system fairer or improve the functioning of the housing market, achieving more than two of those aims at the same time is a real stretch.

Doing all four is near impossible – and that’s before we even get to the welfare side of the Budget and the looming questions about Local Housing Allowance, the benefit cap and the two-child limit.

Read the rest of this entry »A sheepish Conservative manifesto that misses the target

Posted: June 11, 2024 Filed under: Fire safety, Help to Buy, Home ownership, Homelessness, Housebuilding, Leasehold, Stamp duty | Tags: Conservatives Leave a commentOriginally written as a column for Inside Housing

Wounded by the D Day furore and badly behind in the polls, the Conservatives have retreated to their home ownership comfort zone in their election manifesto.

Rishi Sunak replayed their greatest hits in a Telegraph op-ed overnight and boasted in his speech at the launch that: ‘From Macmillan to Thatcher to today, it is we Conservatives who are the party of the property-owning democracy in this country.’

But he is well aware that the old tunes will be not be enough to fix the multiple housing crises that have developed over the last 14 years. Especially as his government has fallen badly short of the promises it made at the last election in 2019.

Read the rest of this entry »Taxing questions

Posted: November 10, 2022 Filed under: Home ownership, Land, Stamp duty, Tax Leave a commentOriginally written as a column for Inside Housing.

Around £50 billion worth of austerity looks inevitable in next week’s Autumn Statement but it remains to be seen how chancellor Jeremy Hunt will strike the balance between spending cuts and tax rises.

Even if recent reports that suggest he will increase benefits and pensions in line with prices prove to be correct, there are still big questions over local housing allowance (still frozen despite rising rents) and the benefit cap (which will catch thousands more tenants if the thresholds stay frozen) and housing budgets already eroded by inflation look vulnerable to cuts in capital spending.

On tax, the stamp duty cut was one of the few measures proposed in the mini-Budget in September that has survived the demise of Liz Truss and Kwasi Kwarteng. So far at least.

But there has been very little debate about where the tax burden should really fall, and in particular about the balance between taxes on income and taxes on wealth.

Read the rest of this entry »Kwarteng’s plan causes growing pains

Posted: September 23, 2022 Filed under: Budget, Cost of living, Housing market, Stamp duty | Tags: Conservative Party, Kwasi Kwarteng Leave a commentOriginally written as a column for Inside Housing.

So, after 10 years of redistribution and socialism under David Cameron, Theresa May and Boris Johnson, now we know what a proper Conservative government looks like.

The biggest package of tax cuts seen in 50 years will cost a cool £45bn and overwhelmingly benefit the highest earners: someone on £1m a year will be around £55,000 better off next year.

The benefits get progressively smaller the less you earn: someone on £20,000 a year will gain just £218 while someone on £200,000 will gain £4,333.

And there is nothing so far for the very poorest: no more help for renters and no boost to Universal Credit.

Instead around 120,000 claimants face having their benefits cut unless they find more part-time hours from January.

There may be some announcements still to come in an actual Budget to follow this Growth Plan, including vital decisions on whether to unfreeze Local Housing Allowance and the benefit cap, but the contrast could hardly be more stark.

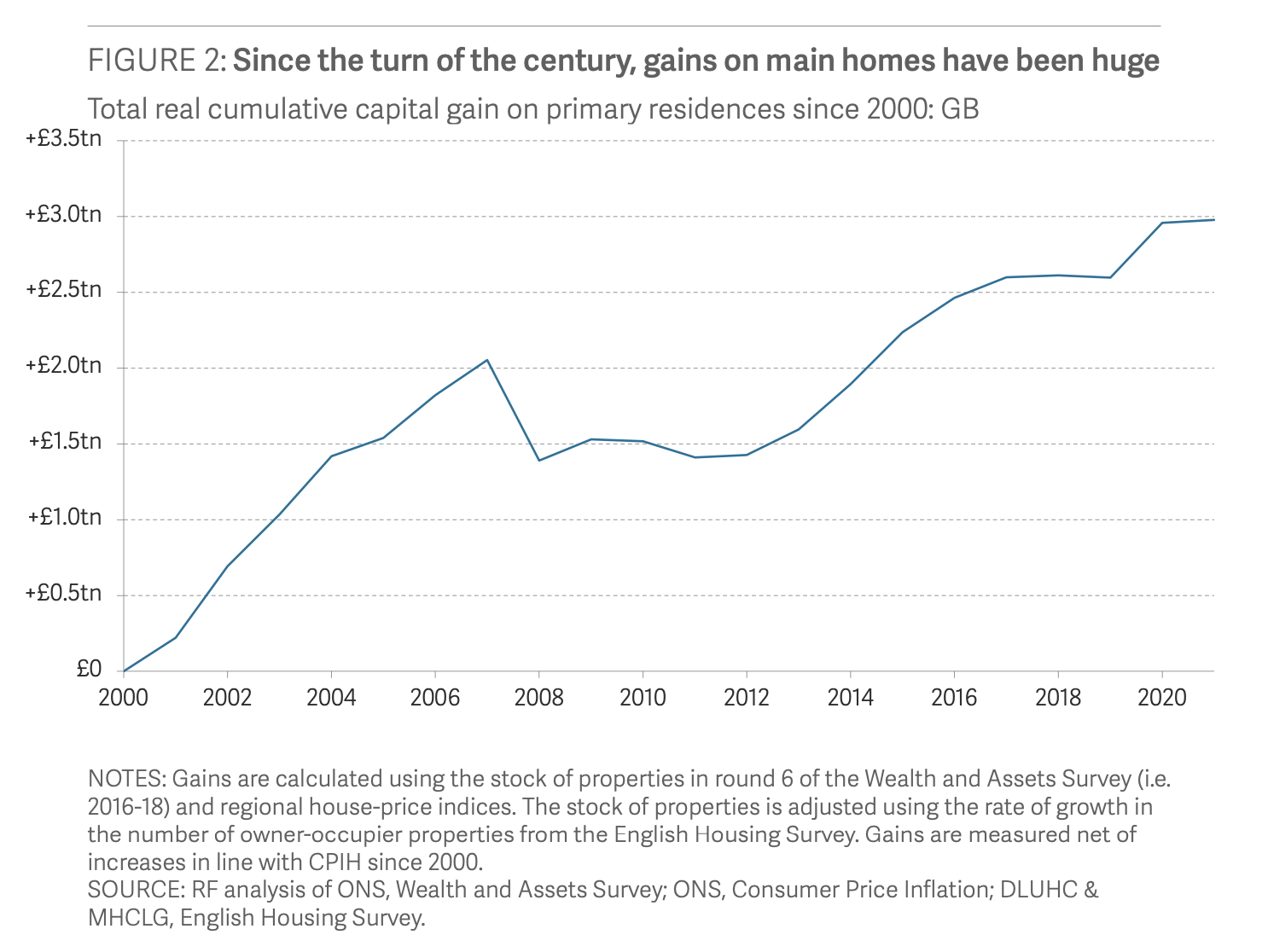

Read the rest of this entry »The £3 trillion question

Posted: December 10, 2021 Filed under: Housing market, Inequality, Tax | Tags: Resolution Foundation Leave a commentOriginally written as a column for Inside Housing.

It has so many zeros in it that it’s worth writing it out in full: £3,000,000,000,000.

That’s the increase in the housing wealth of British households since 2000, according to new analysis from the Resolution Foundation. Perhaps even more remarkably, as the graph below shows, around half of that has been (un)earned since 2012, in the wake of a Global Financial Crisis that seemed set to bring the whole market crashing down.

The distribution of all that housing wealth has been startlingly unequal. Londoners gained almost four times as much (£76,000) as those in the North East (£21,000) and the over-65s eight times as much as 30-34 year olds and more than three times as much as 35-39 year olds.

Where the least wealthy third of households gained less than £1,000 per adult, the wealthiest 10 per cent chalked up an average gain of £174,000.

Needless to say, the gains for anyone who has remained a social tenant or a private renter are zero and zero – and less than zero for leaseholders unlucky enough to be stuck in unmortgageable and unsaleable flats.

Read the rest of this entry »