The £3 trillion question

Posted: December 10, 2021 Filed under: Housing market, Inequality, Tax | Tags: Resolution Foundation Leave a commentOriginally written as a column for Inside Housing.

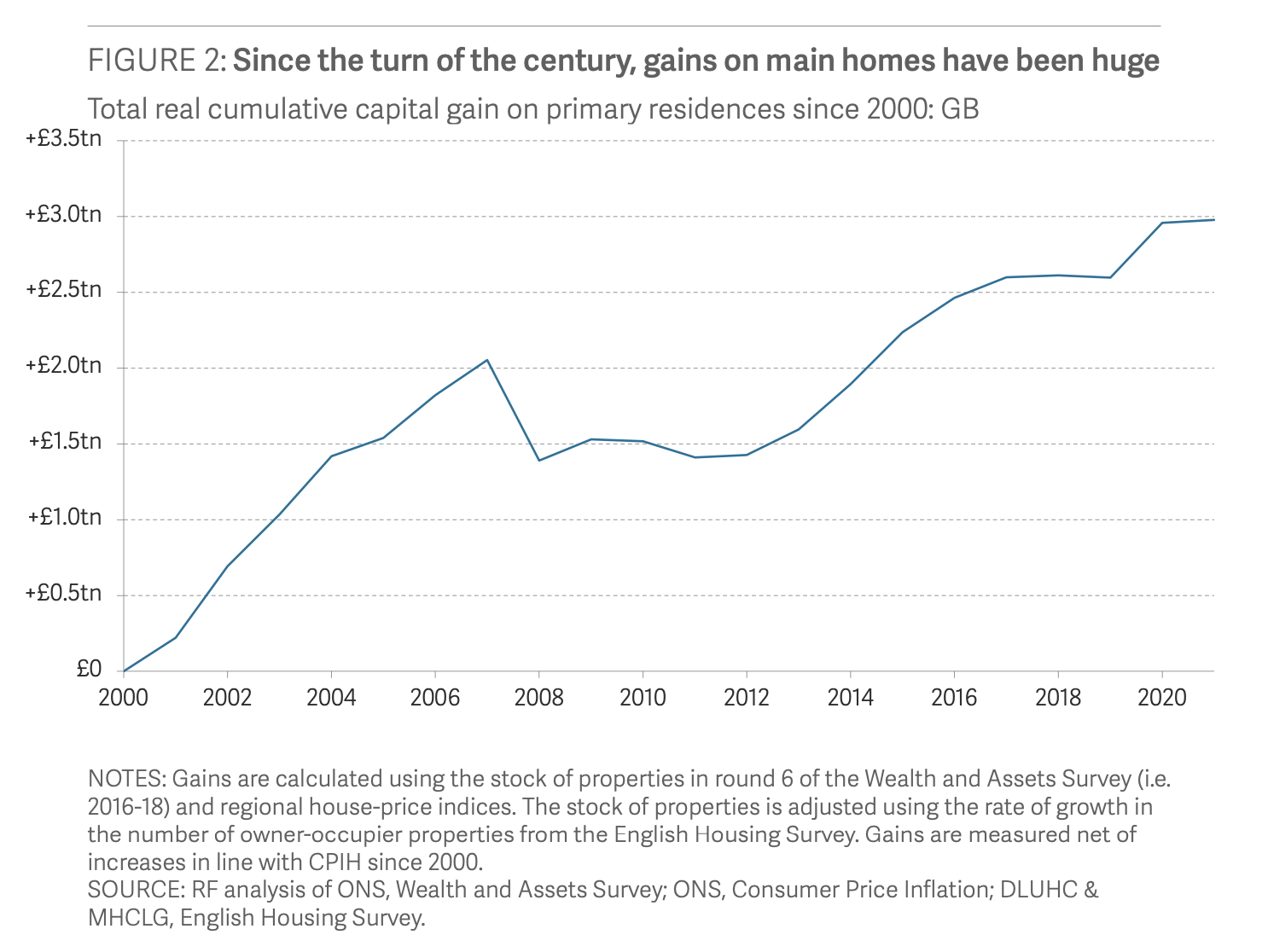

It has so many zeros in it that it’s worth writing it out in full: £3,000,000,000,000.

That’s the increase in the housing wealth of British households since 2000, according to new analysis from the Resolution Foundation. Perhaps even more remarkably, as the graph below shows, around half of that has been (un)earned since 2012, in the wake of a Global Financial Crisis that seemed set to bring the whole market crashing down.

The distribution of all that housing wealth has been startlingly unequal. Londoners gained almost four times as much (£76,000) as those in the North East (£21,000) and the over-65s eight times as much as 30-34 year olds and more than three times as much as 35-39 year olds.

Where the least wealthy third of households gained less than £1,000 per adult, the wealthiest 10 per cent chalked up an average gain of £174,000.

Needless to say, the gains for anyone who has remained a social tenant or a private renter are zero and zero – and less than zero for leaseholders unlucky enough to be stuck in unmortgageable and unsaleable flats.

Interest rates are one of the major factors behind those extraordinary overall gains, first as they fell in the wake of Bank of England independence and inflation targeting after 1997, then again as they fell to record lows after the financial crisis.

But taxation is another. Stamp duty is the main tax on home ownership and rates have risen sharply but it is paid by buyers rather than sellers and it goes with the flow of existing wealth.

Council tax is theoretically linked to house prices, but valuations have not been updated since 1993 and households some of the wealthiest parts of the country have lower bills than more modest ones.

Otherwise, gains in housing wealth are mostly tax-free. Unlike other forms of investment, principal residences are not subject to Capital Gains Tax (CGT), an open invitation to borrow as much as possible and buy as expensive a home as you can afford.

Homes are subject to inheritance tax (IHT) but, thanks to concessions introduced by George Osborne even as he cut benefits, up to £1m can be passed on tax free. That means that most estates are not taxed and housing inheritances fuel intra- as well as inter-generational inequality.

Recent reforms advertised as ‘fixing’ social care in reality only fix the problem of having to sell your home to pay for personal care costs in a way that disproportionately benefits home owners in the South East.

All that unearned income therefore goes largely untaxed even as taxes on earned income are set to rise to the highest levels seen since the Second World War in the wake of the last Budget.

The Resolution Foundation is calling for a debate on that focussing on CGT and IHT, but any reform would be politically controversial to put it mildly.

The think tank puts forward a series of options that could raise between £4 billion and £11 billion a year and compares these to the costs of raising the National Insurance threshold to £12,500 as in the last Tory manifesto (£6 billion a year), giving a £10,000 grant to everyone at 25 (£7 billion) and building 60,000 new social homes a year (£6 billion).

However, the issues involved are complex. For example, retrospective taxes are generally seen as undesirable but leaving existing housing wealth untouched would miss the point.

The Resolution Foundation’s solution to that is to apply CGT only to gains since 2000 but not to gains that have already been realised. However, that would disproportionately penalise people who bought a house to live in and stayed in it compared to those who treated it as an investment and repeatedly traded up.

Simply applying the existing CGT system to main residences would raise the most money but would deter anyone from moving unless it had roll-over relief built into it.

Such concerns hint at why even debating this issue has been politically taboo until very recently.

Slowly some political space is opening up for ideas like this and for Fairer Share, the campaign to abolish council tax and stamp duty in favour of a proportional property tax.

If reform sounds like a long shot right now, it’s worth thinking back to what happened in the 1980s and 1990s.

Mortgage interest tax relief was also seen as politically untouchable then, even though the tax it was relieving had been abolished in the 1960s and abolition had been recommended by two inquiries led by the Duke of Edinburgh.

However, within 10 years of the resignation of its biggest supporter, Margaret Thatcher, in 1990, mortgage tax relief had been phased out and abolished with support from both main parties (for home owners – it took another 20 years for landlords).

The irony was of course that just as what was seen as a state subsidy for house prices was being abolished, a fresh and tax-free boom was already underway. We are still living with the consequences.