Housing and the cost of living

Posted: September 20, 2023 Filed under: Cost of living, Housing market, Private renting, Rents, Social housing Leave a commentOriginally written as a column for Inside Housing.

Inflation is starting to fall at last but the chances are what you pay for your housing has gone up along with the cost of everything else.

But this week’s inflation figures got me thinking about what we really mean by ‘inflation’ and how rising prices work differently in different tenures.

For starters, it all depends on the measure you use. The Consumer Price Index (CPI) is the one in the Bank of England’s inflation mandate so it matters most to its decisions on whether to raise interest rates or not.

CPI inflation affects the Bank’s decisions on interest rates which in turn drives mortgage rates so it is good news that it fell to 6.7 per cent in the year to August. However, CPI does not include owner-occupiers’ housing costs and it is not the index favoured by the Office for National Statistics (ONS).

If you’re not confused yet, on the ONS’s favoured measure of CPIH (which includes owner-occupier housing costs and council tax) inflation fell to 6.3 per cent in the year to August.

However, those costs are based on an estimate of the equivalent rents that owner-occupiers would be paying. There may be sound economic arguments for excluding rising asset values from the inflation calculation but rising house prices still mean rising housing costs for home owners that are ignored.

Old-style Retail Price Index (RPI) inflation – also falling but still considerably higher at 9.1 per cent – is the only measure that directly includes mortgage interest payments but is seen as less accurate than CPI and is no longer treated as on official statistic by the ONS. Despite that, RPI is still used to set price increases in some leases.

For all the differences between the three measures, it does seem clear that rising costs for renters and owners are playing an increasingly important role in inflation in household costs as the impact of the huge hikes in gas and electricity prices starts to recede. This ONS graph illustrates that only too clearly:

But what is really happening to house prices and rents? It all depends on who you believe.

Read the rest of this entry »30 years after – part 2

Posted: July 3, 2023 Filed under: Help to Buy, Housing associations, Housing market Leave a commentOriginally written as a column for Inside Housing.

Kylie Minogue is riding high in the charts, Frankie Dettori wins the Ascot Gold Cup and the housing market looks to be in deep trouble.

In 1992, as in 2023, the more some things change, the more they stay the same.

Part 1 of this column looked at the similarities and the differences between the situation now and 30 years ago. This second part looks at the potential consequences for the housing system as a whole and what the government can do about it.

Arrears and repossessions: This is the issue burnt into the collective memory from the crash of the early 1990s, with repossessions peaking at 75,000 in 1992 and more than 400,000 owners losing their home in the decade as a whole.

The political impact was huge: the economic doom and gloom may well have contributed to the surprise Conservative victory at the general election in April 1992 but Black Wednesday that September ruined the party’s reputation for economic competence for years to come.

Partly thanks to that experience, and the losses made by lenders then, we are going into this downturn with arrears around half and repossessions about a quarter of the level at the equivalent stage in the 1990s cycle when prices were just beginning to fall.

A repeat currently looks unlikely unless we see second-round effects of sustained rate rises including a recession and large-scale job losses – but the odds on those are shortening.

Read the rest of this entry »30 years after – part 1

Posted: June 22, 2023 Filed under: Buy to let, Housing market, Mortgages Leave a commentOriginally written as a column for Inside Housing.

Interest rates rising to tame inflation. Home owners worrying about how they will pay their mortgage. Politicians panicking about the economic and electoral impact.

Prospects for the housing market arguably look bleaker than at any time since the spectacular crash of the early 1990s (unless you are a renter waiting for prices to fall, of course).

Ultra-low interest rates helped the economy out of the downturn that followed the financial crisis in 2008 and have underpinned rising house prices over the last 13 years. But that whole era now seems to be over and the escape route looks blocked.

So how does the situation now compare to what happened 30 years ago? This first part of a two-part column looks at the similarities – and some significant differences.

Read the rest of this entry »Downturn is a chance for a reset – but will the politicians take it?

Posted: February 27, 2023 Filed under: Affordable housing, Housing market Leave a commentOriginally written as a column for Inside Housing.

Housing market downturns are often dominated by debates about their consequences – whether they be falling house prices and negative equity, arrears and repossessions or builders going bust – and what to do about them.

But an important new report from the Joseph Rowntree Foundation argues that we should be thinking less about house prices and the immediate response to the downturn and more about the housing system as a whole and the long-term opportunities for a reboot.

We are already in a downturn even if the shape of it remains unclear. Toby Lloyd, Rose Grayston and Neal Hudson consider different scenarios ranging from back to normal (rising prices) to an outright crash but think market stagnation is the most likely outcome.

That may sound mild when seen in terms of house prices alone but the consequences would be dire: home ownership would remain inaccessible, driving up private rents and making it even more of a struggle for low-income households to keep a roof over their heads.

Arguably we are already seeing stagnation in housebuildling as the big developers slow down development and the industry as a whole warns that completions could fall to less than half their pre-pandemic peak while blaming government regulations.

The conventional response would be to support supply and boost demand but that would be very much like a rehash of what happened after 2010, when various forms of Help to Buy did increase housebuilding but also produced a boom in housebuilders’ profits, share prices and bonsues without much quid pro quo.

For all the efforts to boost the home ownership chances of first-time buyers, the private rented sector continued to grow. And millions of people in housing need were the losers as austerity put the squeeze on social rent and forced housing associations into affordable rent and market sales.

Read the rest of this entry »The state of the (housing) nation

Posted: November 1, 2022 Filed under: Bed and breakfast, Decarbonisation, Homelessness, Housing market, Levelling up, Private renting, Social housing Leave a commentOriginally written as a column for Inside Housing.

The UK Housing Review Autumn Briefing Paper is published this week and as usual provides an invaluable guide to the state of the housing nation. Here are five graphs that illustrate key points about five different parts of the housing system:

Shifting rules on rents

What everyone wants to know, of course, is what will come in place of that purple line on the right but the graph is a reminder that so-called long-term deals on social housing rents can quickly disappear. The four-year rent reduction at the end of the 2020s that ended the previous one is now set to be succeeded by an annual increase significantly below the 11.1 per cent implied by the CPI plus 1 formula.

The decision is finely balanced between cost of living considerations and housing investment, with the existence of housing benefit making it much more complex than it was in the famous case of Clay Cross 50 years ago.

The Briefing Paper quotes estimates by Savills that a 5 per cent cap on rents in England (the government’s favoured option) would cost councils £500 million and housing associations up to £1 billion. One association says that even a 7 per cent cap would mean a 21 per cent reduction in new build and there are also major concerns about the impact on investment in existing stock and on supported housing.

A cap would help tenants not on housing benefit but the major beneficiary would be the Department for Work and Pensions unless its savings are reinvested in housing.

That point was really brought home to me when I interviewed the Welsh housing minister recently. She was only too aware that the more she restricts next year’s rent increase, as might be her instinct, the more savings will go straight back to Westminster, with zero chance of them coming back to Wales.

Read the rest of this entry »Kwarteng’s plan causes growing pains

Posted: September 23, 2022 Filed under: Budget, Cost of living, Housing market, Stamp duty | Tags: Conservative Party, Kwasi Kwarteng Leave a commentOriginally written as a column for Inside Housing.

So, after 10 years of redistribution and socialism under David Cameron, Theresa May and Boris Johnson, now we know what a proper Conservative government looks like.

The biggest package of tax cuts seen in 50 years will cost a cool £45bn and overwhelmingly benefit the highest earners: someone on £1m a year will be around £55,000 better off next year.

The benefits get progressively smaller the less you earn: someone on £20,000 a year will gain just £218 while someone on £200,000 will gain £4,333.

And there is nothing so far for the very poorest: no more help for renters and no boost to Universal Credit.

Instead around 120,000 claimants face having their benefits cut unless they find more part-time hours from January.

There may be some announcements still to come in an actual Budget to follow this Growth Plan, including vital decisions on whether to unfreeze Local Housing Allowance and the benefit cap, but the contrast could hardly be more stark.

Read the rest of this entry »The £3 trillion question

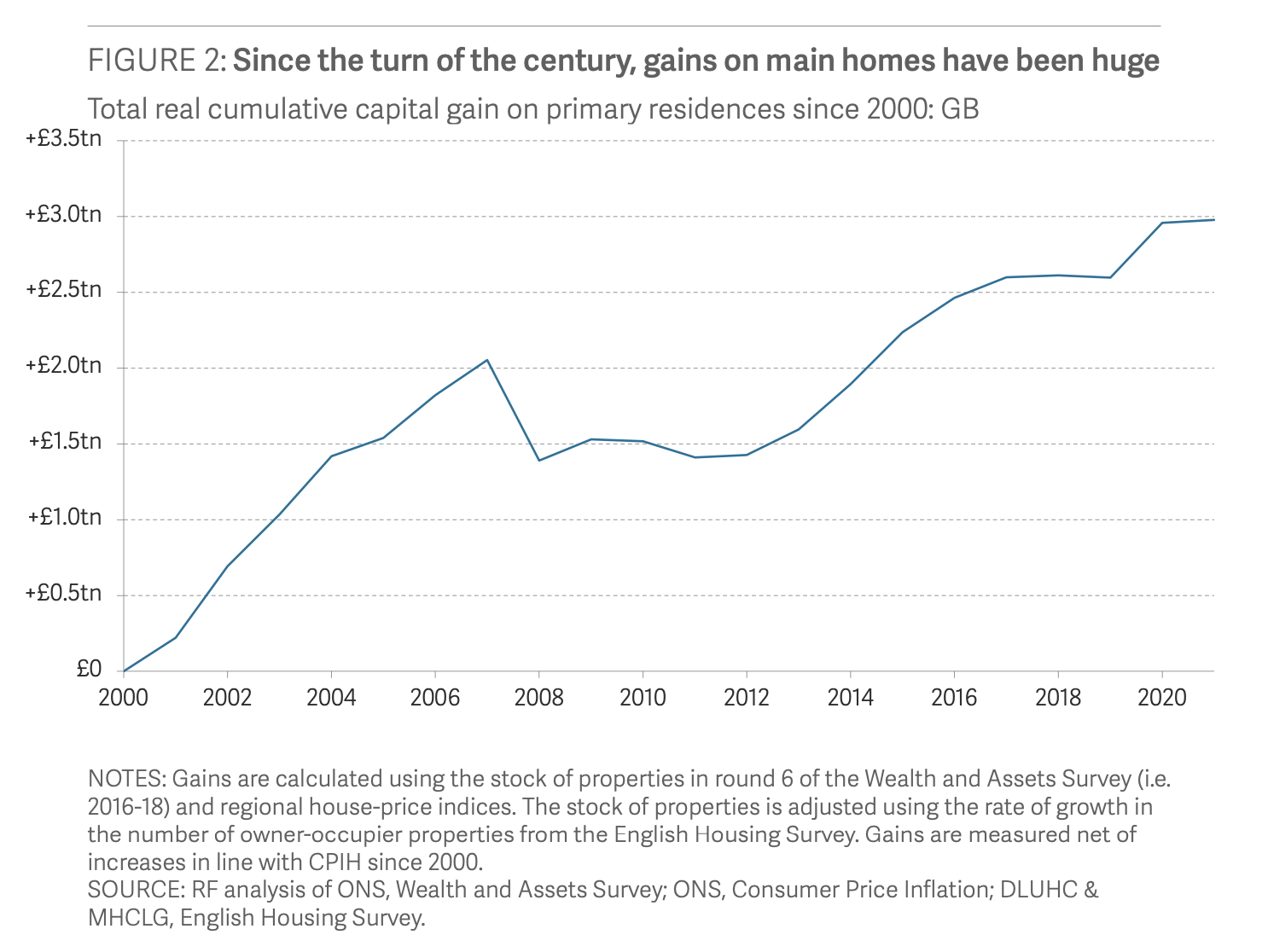

Posted: December 10, 2021 Filed under: Housing market, Inequality, Tax | Tags: Resolution Foundation Leave a commentOriginally written as a column for Inside Housing.

It has so many zeros in it that it’s worth writing it out in full: £3,000,000,000,000.

That’s the increase in the housing wealth of British households since 2000, according to new analysis from the Resolution Foundation. Perhaps even more remarkably, as the graph below shows, around half of that has been (un)earned since 2012, in the wake of a Global Financial Crisis that seemed set to bring the whole market crashing down.

The distribution of all that housing wealth has been startlingly unequal. Londoners gained almost four times as much (£76,000) as those in the North East (£21,000) and the over-65s eight times as much as 30-34 year olds and more than three times as much as 35-39 year olds.

Where the least wealthy third of households gained less than £1,000 per adult, the wealthiest 10 per cent chalked up an average gain of £174,000.

Needless to say, the gains for anyone who has remained a social tenant or a private renter are zero and zero – and less than zero for leaseholders unlucky enough to be stuck in unmortgageable and unsaleable flats.

Read the rest of this entry »