The state of the (housing) nation

Posted: November 1, 2022 Filed under: Bed and breakfast, Decarbonisation, Homelessness, Housing market, Levelling up, Private renting, Social housing Leave a commentOriginally written as a column for Inside Housing.

The UK Housing Review Autumn Briefing Paper is published this week and as usual provides an invaluable guide to the state of the housing nation. Here are five graphs that illustrate key points about five different parts of the housing system:

Shifting rules on rents

What everyone wants to know, of course, is what will come in place of that purple line on the right but the graph is a reminder that so-called long-term deals on social housing rents can quickly disappear. The four-year rent reduction at the end of the 2020s that ended the previous one is now set to be succeeded by an annual increase significantly below the 11.1 per cent implied by the CPI plus 1 formula.

The decision is finely balanced between cost of living considerations and housing investment, with the existence of housing benefit making it much more complex than it was in the famous case of Clay Cross 50 years ago.

The Briefing Paper quotes estimates by Savills that a 5 per cent cap on rents in England (the government’s favoured option) would cost councils £500 million and housing associations up to £1 billion. One association says that even a 7 per cent cap would mean a 21 per cent reduction in new build and there are also major concerns about the impact on investment in existing stock and on supported housing.

A cap would help tenants not on housing benefit but the major beneficiary would be the Department for Work and Pensions unless its savings are reinvested in housing.

That point was really brought home to me when I interviewed the Welsh housing minister recently. She was only too aware that the more she restricts next year’s rent increase, as might be her instinct, the more savings will go straight back to Westminster, with zero chance of them coming back to Wales.

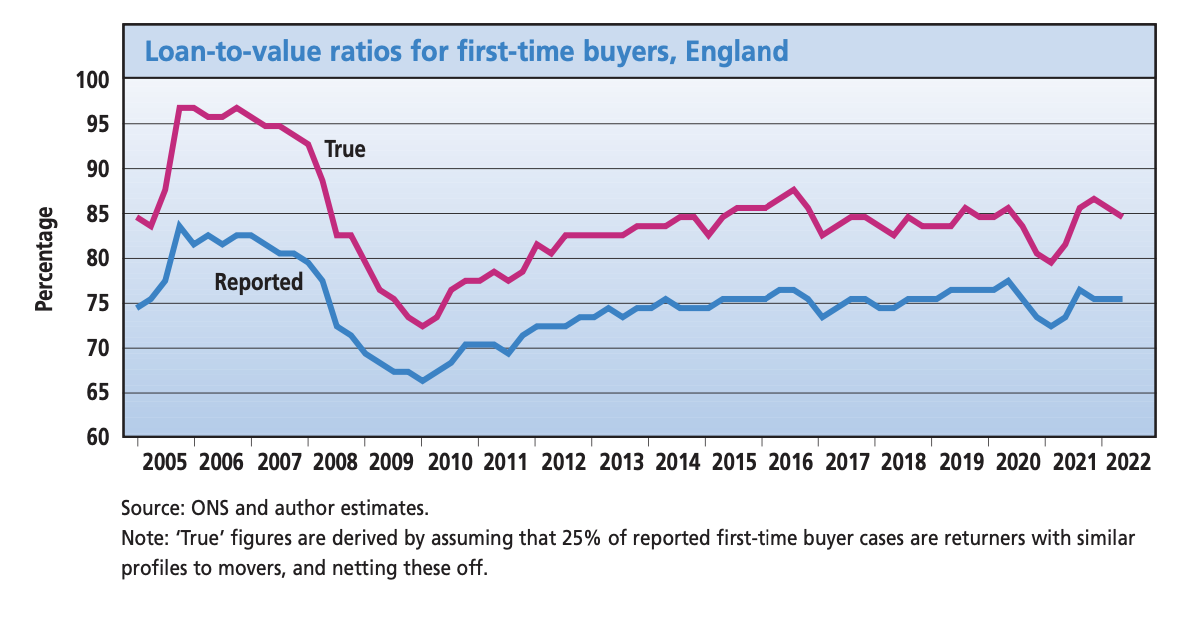

Counting first-time buyers

Ask a Westminster minister about the housing market over the last few months and it’s a fairly safe bet that they will reply with a reference to the fact that first-time buyer numbers climbed above 400,000 in 2021 for the first time since the financial crisis.

However, it’s not as simple as that, says a piece in the Briefing Paper by consultant Bob Pannell since it depends what you mean by first-time buyers. Some are the traditional young families buying their first home but at least 40 per cent of the ‘first-time buyers’ seen since 2021 are actually older people returning to the market armed with much bigger deposits.

The blue line in the graph shows reported loan-to-value ratios for first-time buyers but the red line shows the much greater ratios for ‘true’ first-time buyers (ie those buying for the first time).

At the launch event, Peter Williams highlighted the ‘remarkable resilience’ of a housing market in which many people have continued to do well.

However, he also discussed the severe recent disruption seen in the mortgage market. The good news is that mortgages are now affordability stress tested for higher rates, the bad that landlords on interest-only loans are looking to pass on increased costs to tenants in higher rents.

House prices are already falling in real terms but he still rates the chances of a severe fall (20 per cent or more in nominal terms) as unlikely.

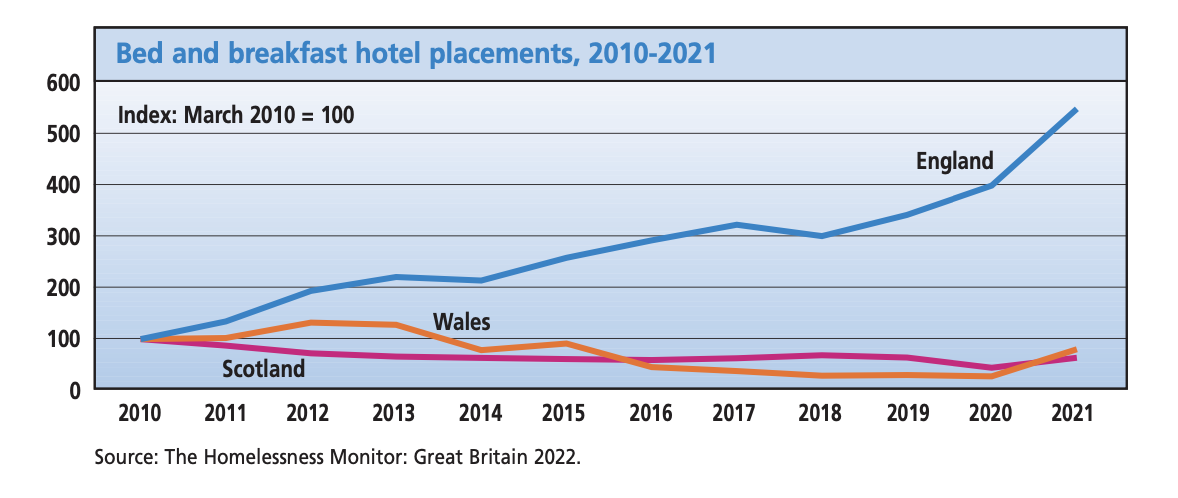

Letting hotels take the strain

Suella Braverman may not like booking them but hotels are still the backstop for all kinds of pressures on the housing system.

The graph shows the depressing rise of bed and breakfast hotels for homeless families, which has risen four times faster in England than in Scotland and Wales since 2010 and has surged again recently. Although, as Francesca Albanese emphasises in the update, use of temporary accommodation is rising significantly in Scotland and Wales too.

Even where help is available there are problems, as last week’s select committee report on exempt accommodation showed only too clearly.

The English government has proclaimed its ambition to be a ‘world leader’ in tackling rough sleeping but, for all the good work being done, recent figures show a 24 per cent increase in rough sleeper numbers in London.

All this comes at a time when, thanks in part to Suella, the system for housing refugees is in crisis. Afghan refugees and thousands of asylum seekers are already stuck in hotels while the Manston camp is bursting at the seams and there are signs of growing stress in the hosting system for Ukrainian refugees.

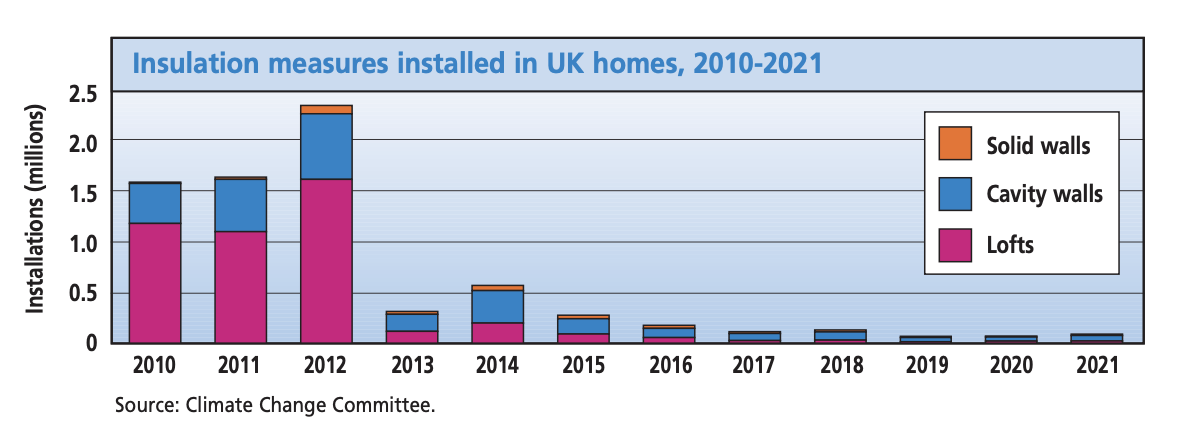

Falling behind on decarbonisation

I’ve highlighted the Climate Change Committee’s verdict on our slow progress on decarbonisation before but it’s worth emphasising again the impact of David Cameron’s decision to get rid of the ‘green crap’ on the number of home insulations carried out after 2012. To deliver on our net zero targets we need to insulate 500,000 homes a year, rising to a million by 2030 but our efforts in the last few years barely register.

There’s better news on new build, with the Future Homes Standard due to be implemented by 2025, but astonishingly we are still building new homes that will need retrofitting later. Meanwhile the Home Builders Federation is already targeting the standard as it lobbies government over the cost of new regulations.

On existing homes, there are impressive sounding targets for the rented stock to meet EPC C levels. Social housing starts from a better position but, as John Perry pointed out at the launch, funding is inadequate. The same is even more true of the private rented sector.

For the owner-occupied stock, there is talk of linking mortgageability to EPC status but little sense that the government is prepared to follow through on something that could break the market for older homes.

A report this week from UK Finance puts the costs firmly into perspective. Upgrading the UK’s housing stock to EPC C would cost an estimated £249.5 billion. There is still no sense there is a strategic plan on anything like the scale required – or even any kind of plan.

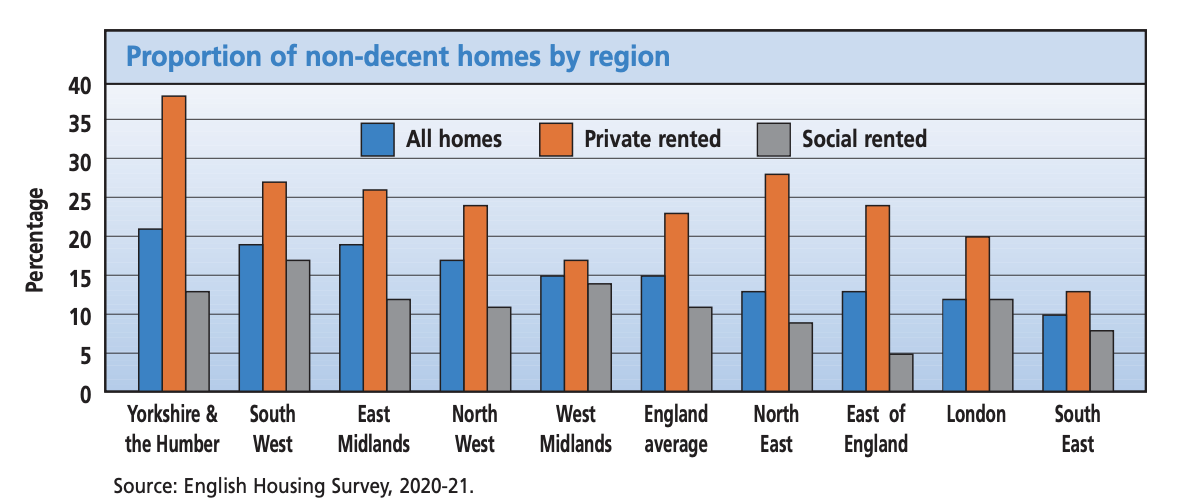

Levelling up decent homes

The government is still apparently committed to levelling up and now free of Liz Truss’s promise to do it ‘in a Conservative way’.

The graph shows one part of the challenge in housing in England: the commitment in the levelling up white paper to apply a decent homes standard to the private rented sector for the first time alongside the target to halve the number of non-decent homes by 2030.

As the update points out, this is a bigger issue the further away from the South East you go. In Yorkshire and the Humber almost four out of ten private rented homes are non-decent.

With Michael Gove back as housing secretary, the hope is that the government remains committed to levelling up but it very much remains to be seen how (and even if) it will apply the standard.

This has obvious links to decarbonisation in terms of whether ambitious targets for improvements are really deliverable.

However, it also links to homelessness, as severe shortages of private rented homes are already being reported in many cases and making it more and more difficult to move people on from temporary accommodation. These shortages will only be exacerbated if landlords decide to sell their properties rather than improve them. The same point obviously applies to social landlords and social housing (and did in the first round of decent homes).

The 2022 UK Housing Review Autumn Briefing Paper can be downloaded here.