Questions that will not go away

Posted: March 31, 2020 Filed under: Affordable housing, Social housing | Tags: UK Housing Review 1 CommentOriginally posted on March 31 as a blog for Inside Housing.

Some time in the long distant past (two weeks ago) we were just emerging from a Budget that signalled better times ahead for affordable housing but left a string of unanswered questions ahead of the Spending Review in the Autumn.

Nest week should have seen the launch of the UK Housing Review 2020 but it appears virtually instead this week in our newly shrunken world as a powerful reminder that other things once mattered.

As ever, it combines a wealth of authoritative statistics about housing with in-depth analysis of all tenures as well as finance, the economy, homelessness, help with housing costs and international comparisons.

What really struck me me is the picture that emerges of the state of our affordable housing and the stark contrast between England and the other UK nations that has developed over the last ten years. This is not new of course but seeing it all brought together is what really hits home.

A detailed scorecard of planned government support for housing investment in England over the next five years shows that 75 per cent of it (£71 billion) will be pumped into the private market via schemes like Help to Buy, the Housing Infrastructure Fund and Home Building Fund.

That leaves just 25 per cent (£18 billion) for affordable housing via the Affordable Homes Programme and initiatives like the Affordable Homes Guarantee Scheme and the removal of HRA borrowing caps.

This is not just the legacy of austerity but of political choices. The other UK nations are subject to the same overall fiscal framework but that has not stopped Scotland allocating 85 per cent of its capital support to affordable housing, Wales 74 per cent and Northern Ireland 100 per cent.

These figures do not include the increase in the Affordable Homes Programme announced in the Budget but what they show is the low base from which those promises are building.

The contrast in what has actually been delivered is just as stark. This graph shows the number of affordable homes delivered in each UK nation adjusted for their population:

On this basis England is completing affordable homes at around half the rate they are managing in Scotland – although cash-strapped Wales is lagging slightly further behind.

And even that comparison takes no account of the meaning of ‘affordable’ in the different nations.

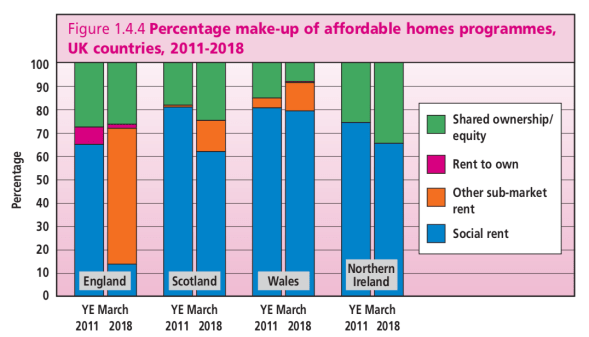

This graph starkly illustrates the impact of changed priorities within England compared to the three other UK nations between 2011 and 2018, and the orange bar highlights just how far affordable took over from social rent south and east of the border.

And that comparison of new homes built takes no account of the differential disappearance of existing social housing stock

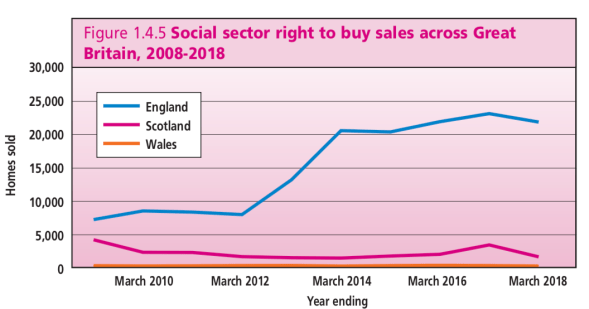

This graph shows the huge divergence in Right to Buy sales between England, Scotland and Wales since 2008:

Look beyond sales and since 2012 England has seen a net loss of 181,000 social rent homes through the Right to Buy, conversions to Affordable Rent and demolitions.

And the latest official figures show that additional sales since discounts were increased continue to outstrip the long promised, never delivered one-for-one replacements.

This is not a new story, and at least the conversion of social rent homes to higher rents has gone into sharp decline, but it does show the starting point for those promises of a £3 billion increase in the Affordable Homes Programme in the Budget and the potential impact of that signal that all new homes will be subject to the Right to Shared Ownership.

Consider too another insight gleaned from the UKHR. In 2018/19, Section 106 contributions with nil grant accounted for 3,572 of 6,287 social rent completions, 12,727 out of 29,135 for Affordable Rent and 9,026 out of 17,024 completions for shared ownership.

All of these could now come under threat from proposals to fund the new First Homes scheme through developer contributions.

Finally, think through the implications of a chapter on funding for housing associations that highlights not just the immediate costs of fire safety work and looming ones of decarbonisations but the rise of for-profit providers and the way that reliance on cross-subsidy was coming under pressure even before the events of the last two weeks.

The signals had at least pointed to more investment in affordable homes – and the case for that was powerfully underlined in the final report from the Affordable Housing Commission last week. Its chair, Richard Best, argues powerfully that the outbreak only underlines the importance of its recommendations.

Such was the world before it was turned upside down by the Coronavirus, with evictions blocked, Local Housing Allowance increased and rough sleepers housed for now and the housing market closed down for who knows how long.

All the signs point to us being stuck in our homes (if we have one) for at least another three months and it could be six months of more before things return to anything like normality.

When we do finally emerge from our isolation, none of these structural problems will have gone away. Can we replace temporary fixes with permanent solutions?

The UK Housing Review 2020 is published by the Chartered Institute of Housing with support from many different sponsors. Copies are available (PDF only for now) here. The main UKHR website is here.

The answer, is very simple, Stop, or severely adjust the ‘ Right to Buy ‘ !